by Thomas Johnson

Often called an “RRSP Meltdown” or a “RRIF Meltdown”, a “Meltdown” strategy is, simply put, a tax and financial planning concept for rapidly liquidating a registered investment account. For example, an individual who redeems a significant portion of their registered assets over the course of a few years rather than attempting to ration the funds over their lifetime.

Why would a person decimate their retirement savings on purpose? What would be advantages and disadvantages of a meltdown strategy? Today, we’ll explore why it’s used and when it may be appropriate for your situation.

Registered money has some serious tax and estate implications. If you own some registered investments (RRSPs, RRIFs, LIRAs, etc…), you’re likely aware of the income tax consequences associated with these accounts. Given that they were funded with pre-tax dollars, the time to pay CRA is when you make redemptions. If you pass away with registered investments, and don’t bequeath them to a spouse, the entire pot will be taxed all at once on your final tax return too. This makes strategic planning around withdrawals paramount to keeping more money in your family’s pocket and paying less in tax.

Drawing down on registered money in low income years is ideal. In Manitoba, in 2021, you can earn up to $9,936 without paying a dime of provincial income tax. You can also earn up to $13,808 without paying federal income tax, thanks to Basic Personal Amounts. If you have no other income to report for the year, drawing on your registered assets to maximize these tax breaks is a fantastic tax planning strategy. Better yet, if you don’t need the funds right away, you can stash the cash in after-tax accounts to hold on for another year.

Registered minimums might not fit into your tax plans. If you own registered accounts, you must convert them into income-producing account types (e.g. RRSP converts to a RRIF) prior to the end of the year you turn 71. You must start receiving a minimum income payment the year you turn 72. If you forecast out your retirement income streams and you see a lot of taxable layers: Canada Pension Plan, Old Age Security, a work pension, employment income, etc… AND you tack on large, registered minimums, you could wind up with some tax pain.

So who is a meltdown strategy for? The ideal registered account meltdown is anyone who has accrued registered money and anticipates some years with little-to-no other sources of taxable income. A great example would be a retiree who leaves work at 60, but wants to defer their pensions (CPP, OAS, employment) until 65. From age 60 to 65, they may not have any source of income and their basic personal exemptions would otherwise be wasted. This person could take abnormally large redemptions from their registered accounts over those years to save their future selves from hefty tax bills.

Meltdown strategies aren’t right for everyone. They take careful co-ordination between your Financial Planner and your Tax Accountant to ensure all bases are covered. If a Meltdown strategy is executed properly, you can reduce much of your future tax liability in a smart systematic way! Your future self will thank you.

by Thomas Johnson

I think it’s safe to say that every single Manitoban with retirement on their minds is asking the question, “how do I get more income in retirement?” It’s perfectly logical to try and optimize your financial position, squeezing the most money you can out of your assets. While every person’s financial situation is unique, here are a few general tips that may likely lead to more money in your pocket:

Delay your CPP as long as you can. Canada Pension Plan (CPP) is one of the cornerstones of most Canadian’s retirement plans. What many people don’t understand is that you can choose when you start receiving those payments. CPP can be started anytime between your 60th birthday and your 70th birthday, with “normal retirement age” being 65. For each month prior to your 65th birthday, you’ll have your benefit reduced by 0.6% (to a maximum of 36%). For each month after your 65th birthday, you’ll have your benefit enhanced by 0.7% (to a maximum of 42%).

How does this look in real life? If you’re expecting a $1,000/month CPP payment should you start at 65, you’d receive $640/month if you start at 60 or $1,420/month by waiting to 70. According to Stats Canada, the average 60-year-old is expected to live for another 22.8 years. The pensioner who started at 60? They’ll get $175,872 in that timeframe. The pensioner who started at 65? They’ll get $214,800 in that span. And the pensioner who started at 70? They’ll receive $219,816! Moral of the story, if you have an average life expectancy, it pays to wait on your CPP.

Avoid the OAS “clawback”. One of the biggest detractors from retirement income is the Old Age Security (OAS) clawback threshold. In 2021, that line in the sand is $79,845 of taxable income. For every dollar you earn over that figure, you’ll have $0.15 of your OAS reclaimed. That’s a 15% bonus tax on your income! How do you avoid that threshold? The simplest solution is to be as tax smart with your money as you can. Consider splitting pension income with a spouse, deferring income where possible, or drawing from low-to-no tax resources rather than fully taxable assets. If you are careful with your income management, you can avoid losing out on your well-deserved benefits!

Prioritize flexibility. There’s a lot of value to being flexible with your money and it’s no different in retirement. It’s important you weigh the costs of guarantees against your need for retirement income. Many financial products (pensions, annuities, GICs, certain investments, etc.) promise guarantees in exchange for higher fees or reduced access to your money. If these options become too restrictive, you may find the only guarantee you have is the guarantee that you’re not getting enough income for your retirement! Be sure to read the fine print and consult with an unbiased financial expert before committing your hard-earned money to a restrictive financial product.

There are many strategies to boosting your income in retirement beyond these three. The biggest piece of advice I can give is to start planning for them sooner rather than later. Rushed decisions often lead to less-than-desirable outcomes. Preparing months or even years before you retire will ensure you’re ready to get the most out of your money!

by Thomas Johnson

As one of our province’s largest employers, Manitoba Hydro hires and retires a tremendous number of individuals every year. It’s no wonder the Crown Corporation is able attract new employees with their flexible work schedules (“Hydro Mondays” are a wonderful thing), competitive wages and extensive benefits package. After a long career working with Manitoba Hydro, the transition to retirement can be daunting if you don’t know what to expect. To better prepare for life after Hydro, consider taking these proactive initiatives to save yourself time, money and headaches:

Save Some Retirement Money on Your Own: Manitoba Hydro’s defined benefit pension program is a key cornerstone to any employee’s retirement plan. The key is that it is meant to be a “cornerstone” and not the “foundation, walls, window and ceiling!” Defined benefit pensions are fantastic, but they can feel restrictive in retirement when it’s your only source of income. If you want to take a tropical vacation, put a down payment on a new truck, or renovate your home, you can’t simply dip into your pension to do so.

Consider supplementing your retirement by directing some personal retirement savings into other vehicles, like a Tax Free Savings Account. This will generate a tax-advantaged pot of money you can access as needed, so you aren’t stuck trying to budget and save for larger retirement expenses, in retirement.

Create an Estate Plan BEFORE Retiring: If you have a multi-decade career with Manitoba Hydro, your pension may be the single largest asset you ever create. It’s not uncommon for seasoned employees to have pensions in the high-six or low-seven figures. That pension is, without a doubt, a significant asset for both you and your family. So how would you feel if you passed away suddenly, early on in your retirement, and your family never received another dime from your pension? Or how would you feel if you passed away and Canada Revenue Agency was cut a bigger cheque than your children?

Those are both very real scenarios that can occur if your estate affairs are not in order. Some truly monumental errors in estate planning can’t be undone if you make the wrong choices the day you submit your retirement notice. If you have a spouse, children, or charity you care about, don’t procrastinate on meeting with a Financial Planner and an estate lawyer to devise a strategy that keeps your money where you want it.

Calculate The Taxes: Income tax has a unique ability to appear without warning and disrupt your retirement plans in a number of ways. If you are thinking of commuting your pension into a lump sum, a significant portion may be taxable in the year you do so if you’re not prepared. If your pension income stream is significant, and you start layering on income from Canada Pension Plan (CPP), Old Age Security (OAS) and Registered Retirement Savings Plans (RRSPs), you could find yourself in an unenviable position of high income tax bills or even facing your OAS benefits being clawed back.

Your pension plan does create opportunities for positive tax planning strategies, like splitting pension income with a spouse or claiming the Pension Income Tax Credit. What’s important is that you plan for optimizing the tax efficiency of your retirement plans early, so you’re prepared to make the right moves when the time comes.

Manitoba Hydro offers many, many benefits to their employees; but a fully planned retirement and legacy are responsibilities of the employees themselves. Take some time to be proactive in your plans and you’ll find the right paths to getting the most out of your retirement!

by Thomas Johnson

Many retirees woke up in January, looked at their bank account, and saw less money in there than they expected. Scrolling through the payments, they noticed that their payment from their Life Income Fund (LIF) account was noticeably lower than it was only a month prior. What happened? Where did that money “go”?

Let’s start with the basics. LIFs are a unique instrument for retirement that are formed out of former pension money. When you leave an employer with a pension, for a new job or to retire, you’ll often be given the choice to commute the lump sum value of your pension into a self-managed account. This account is typically called a Locked-in Retirement Account (LIRA) or a Locked-in Retirement Savings Plan (LRSP). These accounts are eventually converted into a LIF (or an annuity) when you’re ready to start receiving an income.

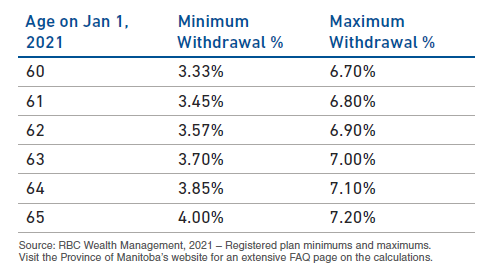

In an effort to keep pensioners from running out of pension funds in retirement, legislators have imposed rules on how much money can be paid out of a LIF account in a given year. There is a legislated minimum that MUST be paid, a legislated maximum that CAN be paid, or you can pick a number in between. The minimums and maximums are most commonly calculated with a simple formula, based on your age at the end of the previous year- the value of your LIF account on December 31st at midnight – and a formula table set out by the government. Here’s a sample of what that looks like in Manitoba:

For a 65 year-old LIF recipient with $300,000 in their account at the end of 2020, they can take an income somewhere between $12,000 (4.00%) and $21,600 (7.20%) in 2021, based on this calculation.

The unique trigger that impacted many LIF recipients in 2021 is a secondary calculation of LIF maximum payments. In Manitoba, your LIF maximum is the higher of the formula above OR the prior year’s investment earnings plus 6% of any new money transferred into the LIF. This nuance meant that pensioners’ 2020 payments were likely buoyed by the big market year that was 2019.

In 2019, the Toronto Stock Exchange (TSX), Canada’s main stock index, rose by about 19%. If your LIF had significant exposure to this index, you may have earned a nice return on your money, which lead to a higher LIF maximum payment in 2020 than you otherwise would’ve received. Instead of the normal, table calculation, your 2020 payments may have been issued based on 2019’s investment performance.

So where did your LIF payment “go”? It hasn’t truly gone anywhere; it’s just returned back to a standard table calculation after being a year removed from hot market performance. What’s the takeaway from this fluctuation? Don’t set up your retirement plans to count solely on a LIF maximum payment! Consider using strategies that bake flexibility into your plans, like unlocking part of your pension or saving in other account types to supplement your retirement income. If you need some help understanding the risks of your pension strategy, consider reaching out to a professional to create game plan that doesn’t catch you off guard!

by Thomas Johnson

If you’ve ever participated in a Manitoba pension in your working career, you may already know that your income options are limited. Government regulations place restraints on “when” you can access your pension income as well as “how much” you are allowed to access in a particular year. If you own a Locked-In Retirement Account (LIRA), as a result of leaving a former employer, this is especially pertinent to you.

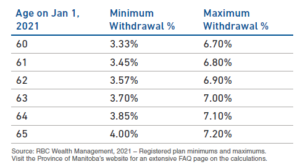

The “normal” course of action for getting at the money inside of a LIRA is to convert it into a Life Income Fund (LIF). LIRA’s aren’t eligible for a direct withdrawal; think of them more as a protective placeholder for your funds, from the time you leave the pension until such time as you’re ready to start an income stream. LIFs, on the other hand, are like turning on a leaky tap. You must take a minimum amount from the LIF each year, yet you can’t take more than a maximum amount either. There’s a “floor” and a “ceiling” and you must have an income somewhere between the two. For example, someone who was 65 years old when 2020 started, had to make withdrawals from their LIF in the 4% – 7.20% range.

The “ceiling” on LIF payments can be very restrictive for many people as they were counting on those pension funds for certain retirement goals. Maybe you want a higher income in early retirement years for travel, vacations, or hobbies. Perhaps you have a specific tax strategy to reduce your registered investments before you begin CPP or OAS. Or maybe you just want the security that you can get at your money if you need it in a pinch. So, what’s a retiree to do?

In Manitoba, we have a very special, very underutilized option to create a Prescribed Retirement Income Fund (PRIF). A PRIF has the same “floor” as a LIF for income requirements, but absolutely no ceiling. You can take as much income as you want from a PRIF in any given year without constraint!

How do I get a PRIF? Each Manitoban can only ever create one PRIF in their lifetime, and it must be created at the same time that you convert your LIRA into a LIF. The most money you can roll into your PRIF is half of the value of your LIRA at that time. That means someone with a $100,000 LIRA can split $50,000 into a PRIF and $50,000 into a LIF. Now only half of their money is subject to a ceiling cap and the other half is far, far more flexible!

Seeing as there’s only one opportunity to create a PRIF, I always recommend the strategy to clients, even if they don’t intend to take advantage. There are no rules stating you must take more from the PRIF than the LIF, but there is definitely a risk that you’ll need access to more money in the future. There is a lot of value in having flexibility with your retirement asset, so don’t miss your chance to create a little more flexibility in your plans!

Recent Comments